-min%20(1).svg)

Your 401(k) and other retirement accounts represent years of hard work and careful planning for your future. When facing divorce, the thought of splitting these assets can feel overwhelming and uncertain.

If you're going through a divorce in Washington State, experienced Spokane divorce attorneys can help you work through the details of dividing retirement funds while protecting your financial security. Here's what you need to know about retirement accounts in divorce.

How Washington State Views Retirement Assets

Washington is a community property state, which means retirement funds earned during your marriage are typically considered shared assets. Any contributions you or your spouse made to a 401(k), pension, or other retirement account during the marriage generally belong to both of you.

When it comes to retirement accounts, timing matters:

- During marriage contributions: All 401(k) deposits, employer matches, and investment growth during your marriage are community property. Courts will calculate the exact marital portion based on when you married and when you're divorcing.

- Pre-marriage savings: Retirement funds from before your wedding day typically stay separate. Money you saved before getting married remains your individual property.

- Mixed accounts: If you had a 401(k) before marriage and continued contributing during marriage, the account will be divided proportionally between separate and marital property.

Community Property vs. Equitable Distribution

While Washington follows community property rules, not every state does. The approach your state takes will significantly affect how your retirement accounts are divided.

Community Property States

In community property states like Washington, marital assets are generally split 50/50. This approach treats marriage as an equal partnership where both spouses contribute equally.

States that follow this model include:

- Washington State: Courts presume equal division of all marital property unless circumstances warrant deviation.

- California, Texas, and others: Several states use this framework for divorce asset division.

- Retirement account impact: Your 401(k) contributions during marriage would typically be split down the middle.

Community property provides a clear starting point, though judges can adjust based on specific circumstances in your case.

Equitable Distribution States

Most states use equitable distribution, which aims for fairness rather than automatic equality. Judges have more discretion to consider individual circumstances.

Key factors courts examine include:

- Marriage length: Longer marriages often result in more equal divisions, while shorter marriages may favor separate property claims.

- Financial circumstances: Each spouse's income, earning capacity, age, health, and economic needs play a role.

- Contributions to marriage: Non-financial contributions like homemaking or supporting a spouse's career are considered.

- Future needs: Courts look at who needs retirement funds more for their post-divorce financial stability.

Equitable distribution gives courts flexibility to craft fair outcomes based on your unique situation. This approach recognizes that equal isn't always equitable when spouses have different financial positions or have made other types of contributions to the marriage.

#cta_start

Get Skilled Guidance on Retirement Assets

Let our experienced Spokane divorce attorneys simplify the process and protect your retirement savings throughout your divorce.

#cta_end

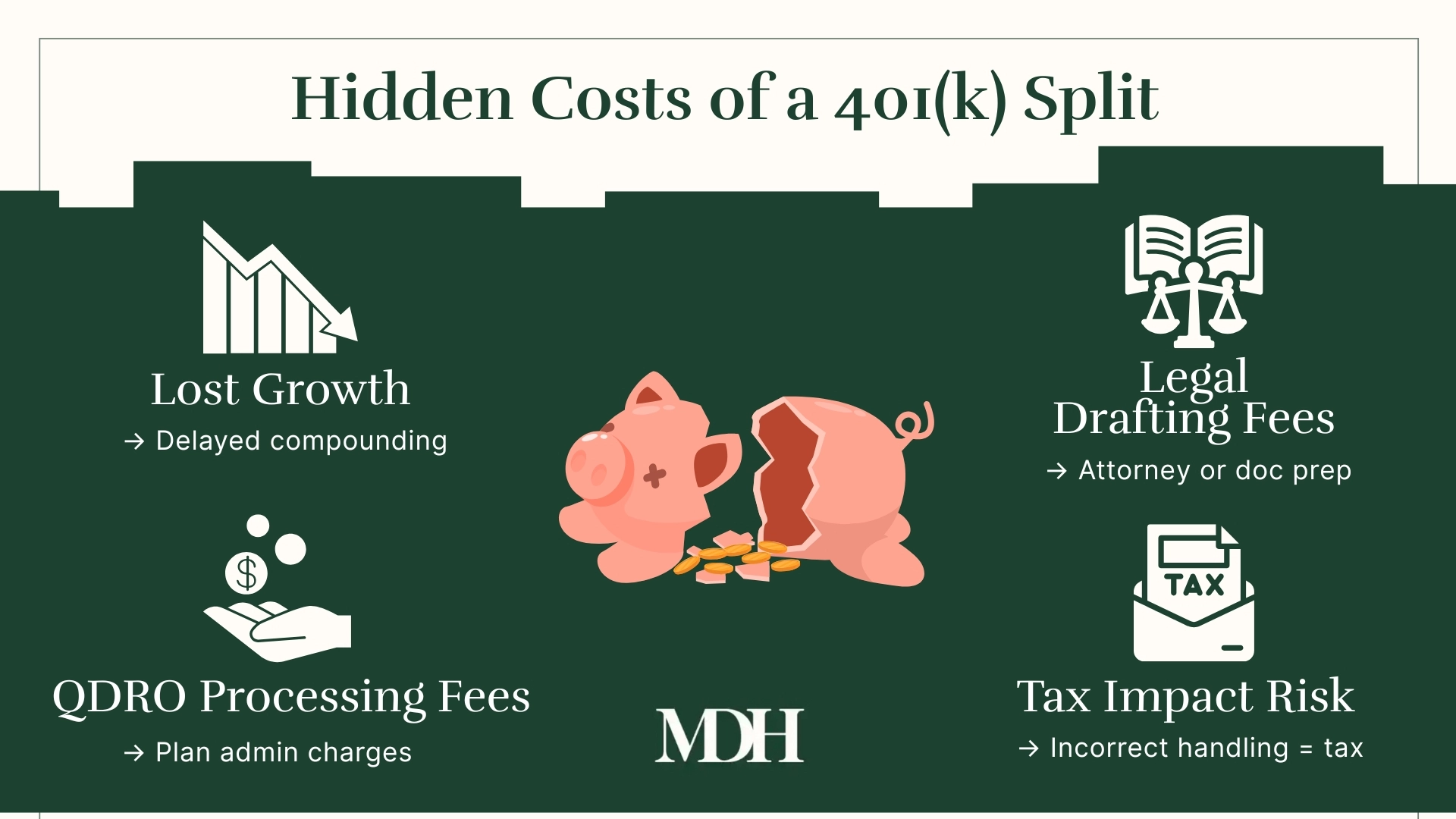

The Role of a Qualified Domestic Relations Order

A Qualified Domestic Relations Order (QDRO) is the legal document that actually divides your retirement accounts. Without a QDRO, your retirement plan administrator won't split your 401(k) or pension.

The order specifies several key details that protect both spouses:

- Amount to transfer: The exact dollar figure or percentage going to your ex-spouse. This prevents confusion and ensures everyone knows what to expect.

- Payment method: Whether funds are transferred immediately or when you retire. Some couples prefer immediate division, while others wait until retirement age.

- Tax treatment: How the transfer will be handled for tax purposes. Proper documentation through a QDRO allows tax-free transfers between spouses.

- Beneficiary rights: What happens if you pass away before retirement? The order clarifies whether your ex-spouse retains any claims to the funds.

QDROs apply only to employer-sponsored plans like 401(k)s and pensions, not to IRAs, which are divided differently under the divorce decree.

Protecting Your Retirement in Divorce

You have several options for handling retirement accounts during divorce proceedings. Each approach has different advantages depending on your situation.

If both spouses have similar retirement savings, you might agree to each keep your own accounts rather than splitting both. This simplifies the process and avoids paperwork. One spouse might keep their full 401(k) in exchange for the other receiving more home equity or other marital property. You can also split retirement accounts based on the percentage earned during marriage, giving each person their proportional share.

Tax Implications You Need to Know

The way you divide retirement funds can have significant tax consequences. Planning ahead helps you keep more of your money and avoid surprises at tax time.

Rolling Over Transfers

Moving your portion into your own 401(k) or IRA avoids immediate taxes. When you do a direct rollover through a QDRO, you won't owe anything until you start taking distributions in retirement. This strategy preserves the tax-deferred status of your retirement savings and gives your money more time to grow.

Avoiding Early Withdrawals

Taking cash now triggers income tax plus potential 10% penalties. Even though divorce allows penalty-free withdrawals under certain circumstances, you'll still owe regular income tax on the amount. The immediate tax hit often makes cashing out one of the most expensive options available.

Considering Withdrawal Timing

Withdrawing funds in lower-income years can reduce your tax burden. If you expect your income to drop after divorce or during a career transition, timing your withdrawals strategically can save thousands in taxes. Planning these decisions with a tax professional helps you make the most tax-efficient choices.

Understanding these tax implications before finalizing your divorce settlement prevents costly mistakes. What seems like an equal split on paper might not be equal after taxes, so factor in the tax consequences when negotiating your settlement.

Other Retirement Accounts in Divorce

While 401(k)s get the most attention, other retirement vehicles also need to be divided. Individual Retirement Accounts (IRAs) don't require a QDRO, but still need proper documentation through the divorce decree. Pension plans can be more complex to value and divide, sometimes requiring actuarial calculations to determine present value. Military pensions are subject to special federal rules under the Uniformed Services Former Spouses' Protection Act and may involve different payment timing requirements.

Securing Your Financial Future After Divorce

Dividing retirement accounts is one of the most important financial decisions in your divorce.

With proper planning and legal guidance, you can protect your retirement security while reaching a fair settlement. Washington's community property laws provide a framework, but you still have options for how to divide assets in ways that work best for your circumstances.

At Hodgson Law Office, we've helped Spokane families work through complex property division matters for over 20 years. Our experienced team will work with you to develop strategies that protect your retirement funds and help you achieve financial stability. Contact us today to schedule a free consultation and take the first step toward securing your financial future.

FAQ

Can I cash out my 401(k) during a divorce?

While you can withdraw funds from your 401(k) during divorce, it's usually not the smartest move financially. You'll owe income tax on the withdrawal, and if you're under 59½, you'll typically face a 10% early withdrawal penalty. A better approach is often to roll your share into another retirement account or negotiate to keep other marital assets instead.

How long does it take to get a QDRO?

The timeline for getting a QDRO typically ranges from a few weeks to several months. It depends on how quickly your attorney can draft the order, how fast the court approves it, and your retirement plan administrator's processing time. Starting the process early in your divorce helps avoid delays in finalizing your settlement.

What if my spouse has already retired and is receiving pension payments?

If your spouse is already collecting pension benefits, you can still claim your share of those payments. The QDRO will specify that you receive a portion of each monthly payment going forward. This is called a "shared payment" approach and continues for as long as your ex-spouse receives benefits.

Do I need to divide retirement accounts equally in Washington?

No, Washington's community property laws don't always require a 50/50 split of retirement accounts. Courts consider factors such as the length of the marriage, each spouse's financial needs, and the overall division of assets when determining what's "just and equitable." You and your spouse can also negotiate any split you both find fair.